Cash mobility . . . in today’s economy, it is more important than ever. But how can corporate treasurers best navigate the complexities of fund movement in and out of restricted markets? Here are some smart insights to help fuel your success.

Head of APAC, Liquidity & Account solutions specialists

By Tim Van Bijsterveldt

Liquidity & Account solutions specialists

By Amy Eckhoff , Tim Van Bijsterveldt

When interest rates rise, corporates often seek to mobilize cash to optimize debt cost and enhance returns. Cash mobility is crucial for self-funding purposes in this unpredictable, global macroeconomic environment. With fungible markets and currencies already tapped into in most cases, companies are now starting to look at freeing up cash from the more restricted markets or enabling funding received in a timely manner to reduce being charged an overdraft rate.

While the U.S. dollar (USD) interest rate is rising, we also notice certain other currencies are increasing, decreasing or becoming and/or remaining relatively volatile. Hedging foreign currency risk thus becomes more important when the corporates access the restricted markets and currencies. These markets often have more restrictions on regulatory controls and cash movement.

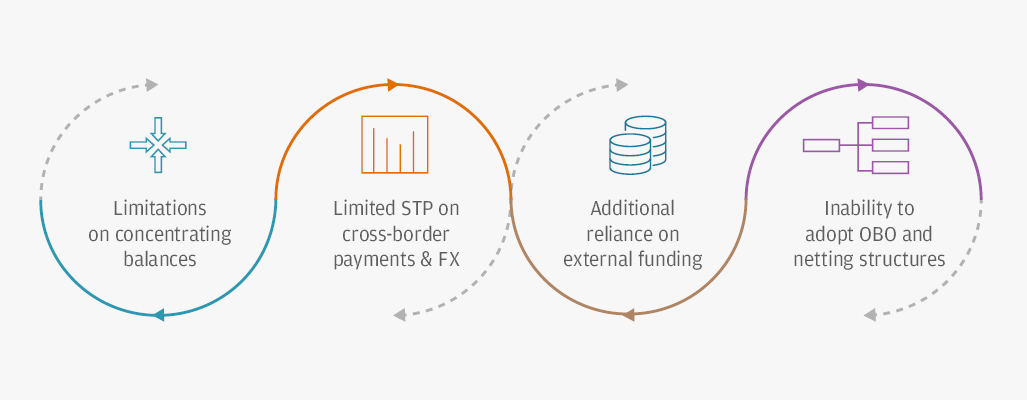

There are other complexities for corporate treasuries dealing with cash in restricted markets:

Limitations on concentrating balances

Limited STP on cross-border payments and FX

Additional reliance on external funding

Inability to adopt OBO and netting structures

Looking back at the liquidity and multicurrency management strategies presented in “Selecting the right strategy to master liquidity challenges in Asia Pacific,” funding can be automated in a foreign currency or across currencies so that funds are made available in-country at the right time and in the right currency. This can take place either via intercompany loans or commercial arrangements, which may not always require regulatory approvals, but the automated funding may still be subject to regulatory reporting or supporting document requirements, such as an invoice.

Extracting cash may be slightly more technical. Often restricted cash can be extracted via intercompany loans, cross-border cash concentration and/or cash/dividend repatriation. As a complement or alternative to cash extraction, excess cash can also be redeployed through alternative methods to enhance returns and onshore payment optimization.

It is important to decide which route to take from the start when funding the respective markets, as this will determine how funds can be taken out.

Decide which route to take from the start when funding the respective markets, as this will determine how funds can be taken out.

Head of APAC, Liquidity & Account solutions specialists

Intercompany loans are one of the most common ways to move funds in and out of a restricted market. Cross-border cash concentration often leverages the intercompany loan framework to move cash in a single currency or across currencies and on an automated basis.

Taking China as an example, we have seen many firms implementing cross-border cash pools for both Renminbi and the USD to mobilize funds in and out of China under the regulatory framework of People’s Bank of China and China’s State Administration of Foreign Exchange. Combined with a notional pooling, this can form a holistic solution to try to mitigate foreign exchange (FX) risks at the regional level and solve currency mismatches.

Funding and extracting cash via intercompany loans can be on an automated or manual basis. While regulatory restrictions may apply, J.P. Morgan supports such intercompany loans for all restricted markets except India, where this is not permitted. While automation is available in most markets for restricted currency conversion, it is advised to do this onshore to benefit from better cut-off times and capabilities. It is also important to consider any potential tax and FX implications attendant to the conversion from the currency of the underlying intercompany loan. Clients are advised to seek the advice of their appropriate adviser or counsel before embarking on any such strategy.

In certain countries, it may be possible to have an intercompany loan denominated in the local currency. This would allow FX exposures to be centralized at the treasury entity. While other regulators only allow the intercompany loan denominated in USD or another foreign currency, they do often allow FX management activities to be centralized with an offshore entity, such as the treasury entity. Prior to cash extraction, it is imperative to make an effort to achieve natural hedging in-country to minimize currency mismatches, optimize operations and maximize the amount of excess cash available.

Dividend repatriation is another tool we have observed corporates adopting to move money out of restricted markets—especially for countries like India and Vietnam, where cross-border cash concentration is not permitted. This could also be a more appropriate solution for cash extraction in case of a structural excess in a similar way that capital injection could be a better solution in case the funding amount is large and the period becomes too long.

Given the significant cash outflow due to a dividend payout, it is important to perform a proper analysis and/or partner with J.P. Morgan to identify appropriate methods for managing risks and FX exposures, including how to minimize slippage on both spot and swap levels on the various hedging solutions selected and selecting the right FX partner and hedging location.

It is important to perform a proper analysis and/or partner with J.P. Morgan to identify appropriate methods for managing risks and FX exposures.

Tim Van Bijsterveldt

Liquidity & Account solutions specialists

Cash can be redeployed to support your investment activities according to a corporate’s

strategic priorities.

Our Unitized Time Deposit (UTD) offering is an automated, end-of-day investment program that deploys your surplus cash in your current accounts into preferred units of call deposits based on your predetermined target balance parameters. If and when funding is required to ensure the operating account(s) remain in a positive balance position, the UTD would break only the units of call deposits to close off the negative position without breakage fees and with a “last-in-first-out” principle. This ensures that idle balances are minimized, while allowing you to maximize yields on your surplus operating balances at optimal cost.

Another alternative is a money market fund, which may enhance yield and could optimize counterparty exposure and risk management—albeit at the cost of being fully liquid.

We observe that companies with a structural excess cash position sometimes redeploy the cash by investing in or acquiring companies via local and/or overseas investments or corporate restructuring. It is important to recognize that, should returns be in other currencies not local to you, translation may pose foreign denominated cash risks. Translation of foreign currency balance sheets and income statements could pose cash and earnings risks.

Often overlooked as part of liquidity optimization is the renegotiation of payment terms that could free up liquidity for a period of time that could either avoid a potential period of deficit, or allow the entity to benefit from yield longer.

Furthermore, should there be a mismatch in payment and functional currencies, transactional FX risks can be managed via hedging strategies. We often see this in large multinationals, where an attempt was made to not have each factory invoice a sales entity in their respective currency by operating in a single currency across the group. This could, however, still cause exposures for the entities in question.

Centralizing the invoicing across the group via a single entity regionally or globally could minimize FX exposure. The central entity could also consider invoicing each respective entity in their functional currency. Not only will individual subsidiaries pay/receive in the respective local currencies, eliminating the need to hedge FX risks at the entity level, it also could open up the automated extraction of trade-related fund flow from restricted markets into the treasury hub.

Before considering the extraction or redeployment of restricted cash as part of a medium- or long-term liquidity and multicurrency management strategy, corporates should define reasons to mobilize cash out of restricted markets—i.e., would that cash be used for self-funding purposes or for an investment? It is also important to define repatriation or redeployment strategies by considering the underlying fund flow, and the implications on tax, FX and accounting.

With J.P. Morgan’s deep knowledge and understanding of restricted markets and currencies, we can help companies attain the most optimal liquidity management solution.

Connect with your J.P. Morgan representative to get started today.

All rights reserved. The statements herein are confidential and proprietary and not intended to be legally binding. Not all products and services are available in all geographical areas. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice or investment recommendations. Visit jpmorgan.com/disclosures/payments for further disclosures and disclaimers related to this content.